Posts Tagged ‘key account management’

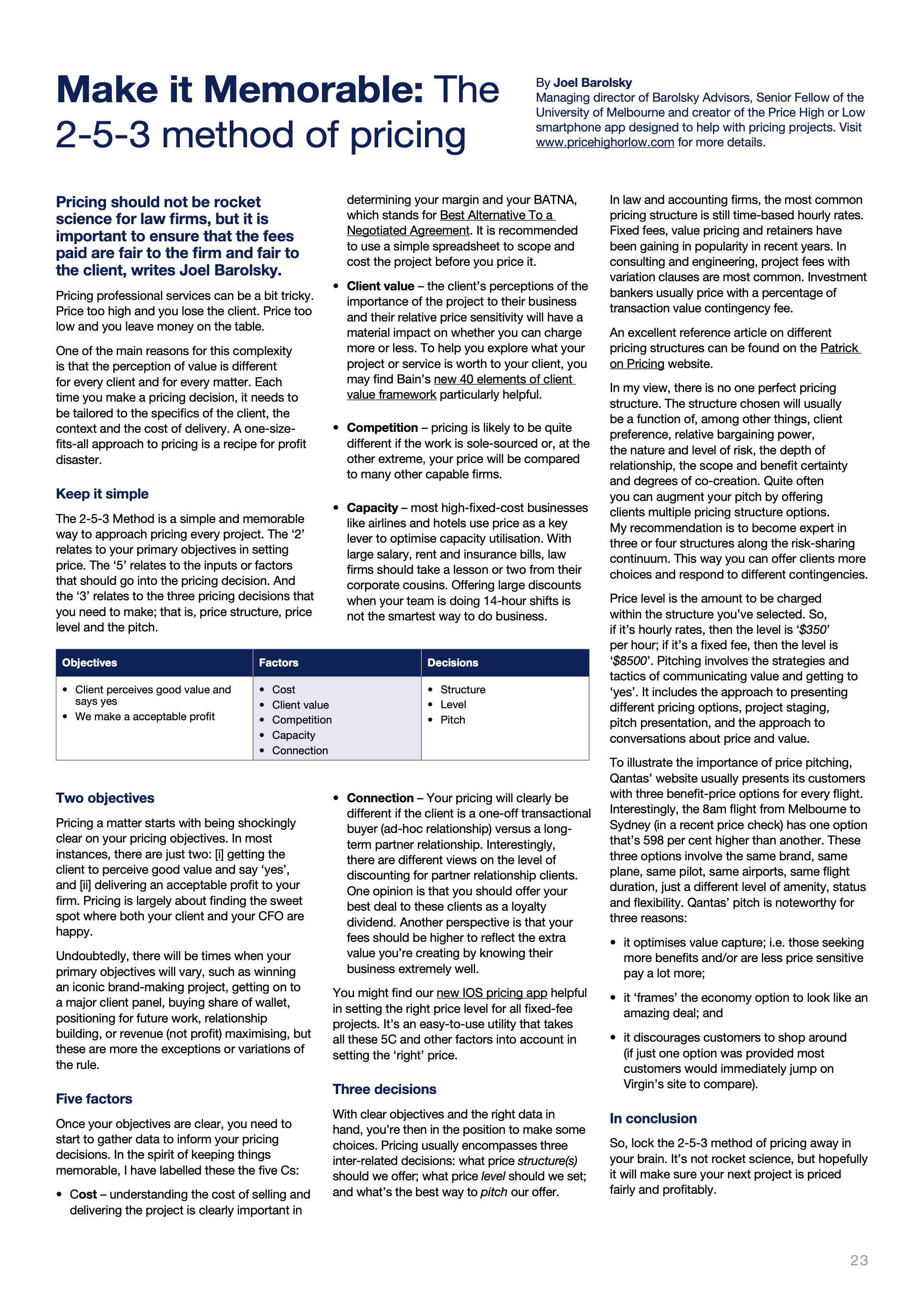

Make it Memorable – my recent article on pricing professional services published in BRIEF

In Articles on 28 July 2020 at 12:21 pmTackle this law firm profit problem or go for a surf

In Articles, Commentary on 5 October 2019 at 9:32 amFull text of an opinion piece first published in the Australian Financial Review on 4 October 2019.

With the march of technology, law firms face a profit problem if two trends persist.

The first trend relates to how firms charge for their services. Recent Acritas data reveals that time-based pricing still predominates across the legal market. This includes both billing retrospectively via hourly rates as well as upfront capped or fixed fee pricing based simply on an estimate of time multiplied by hourly rates.

The second trend relates to investment and advances in legal technology. Over $1.75 Billion has already been invested in new legal technology across the globe in the nine months to September 2019.

The published version of the AFR article

Today, technology is used primarily for email, word processing, legal research and in discrete areas like e-discovery. At a very simplistic level, one could say that software is currently about 5% of the “average” service product.

In five years, sophisticated technology will become integral to service delivery. It will be used legal document preparation, contract review, advice in rules-based legal areas, due diligence, case prediction and in process automation. Many elements of a firm’s IP will be incorporated in smart precedents and algorithms.

As best as we can predict, in five years legal technology will make up roughly 25% of the legal product. This percentage will be much lower in brain surgery practice areas, but higher in volume more commoditised work types.

The profit problem arises because it’s really hard to charge for software in 6-minute increments!

Using the simple percentages noted above, revenue for 25% of the legal product will not be captured if firms just bill or price based on the time that humans are involved.

Moreover, given that much of the new technology is focused on lawyer efficiency, revenue will decrease by having fewer human hours in service delivery. Costs will increase to procure, tailor and deploy software, and in capturing firm IP.

Find a new model

The financial impost will be huge unless law firms find a new model.

Value-pricing is one approach that can be used, in part, to address this problem. Rather that setting fees based on inputs and time, price is set by reference to client perceived benefits. A fee is agreed upfront based on client preferences, context, scope of work and anticipated outcomes, both short- and long-term.

While value-pricing has much appeal, there are constraints on both the supply and demand side. Some lawyers are reluctant to take on the risks of promising outcomes and in fixing fees. Others really struggle to quantify and communicate the value they provide. They prefer selling time as it facilitates practice autonomy and it covers up any inefficiencies. Many law firms have an entrenched culture of using time records to assess productivity.

On the demand side, it appears most large corporate and government clients are very comfortable with the transparency and comparability of conventional time-based methods. They back themselves, or their e-billing software, to critically review proposals and bills, and not pay for any obvious time padding or wastefulness.

Almost every major client panel tender in Australia over the past three years has asked firms to propose “alternative fee arrangements”. Very few clients adopt any of these alternatives and most resort to discounted hourly rates to compare firms and to pay for services rendered.

Enough fat

Some clients view technology, project management and other non-lawyer time as ancillary benefits or ‘value-adds’ that firms have given away in the past and they should not need to pay extra for in the future. They see high hourly rates as having enough fat in them to comfortably cover all the elements that go into service delivery.

So, if the tech wave is unstoppable and hourly rates are entrenched, what options are on the table?

- Do nothing and just wear the cost.

- Focus exclusively on highly complex and bet-the-company matters where rates can be increased to maintain margins.

- Redouble efforts to collaborate with clients to find new pricing models where the total value created is captured and shared fairly. This would include negotiating a mix of time, value-based and technology pricing models including license fees, subscriptions and platform payments.

- Scale-up, merge with competitors and accelerate the adoption of technology and other tools to be the lowest cost provider and have more price-setting discretion.

- Close-up shop and go surfing.

Feel like a surf, or are you up for the challenge?

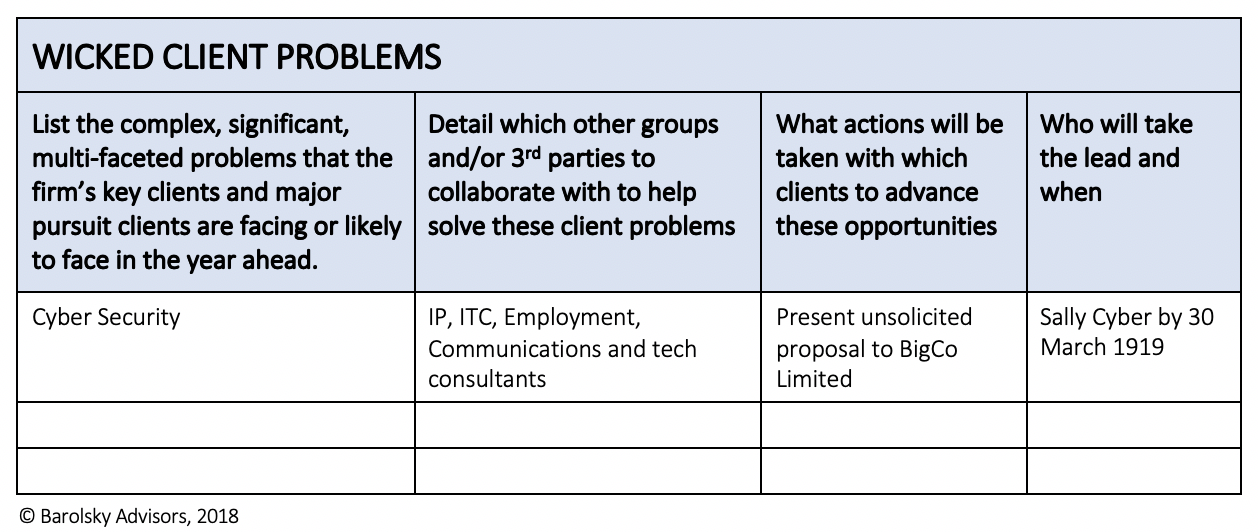

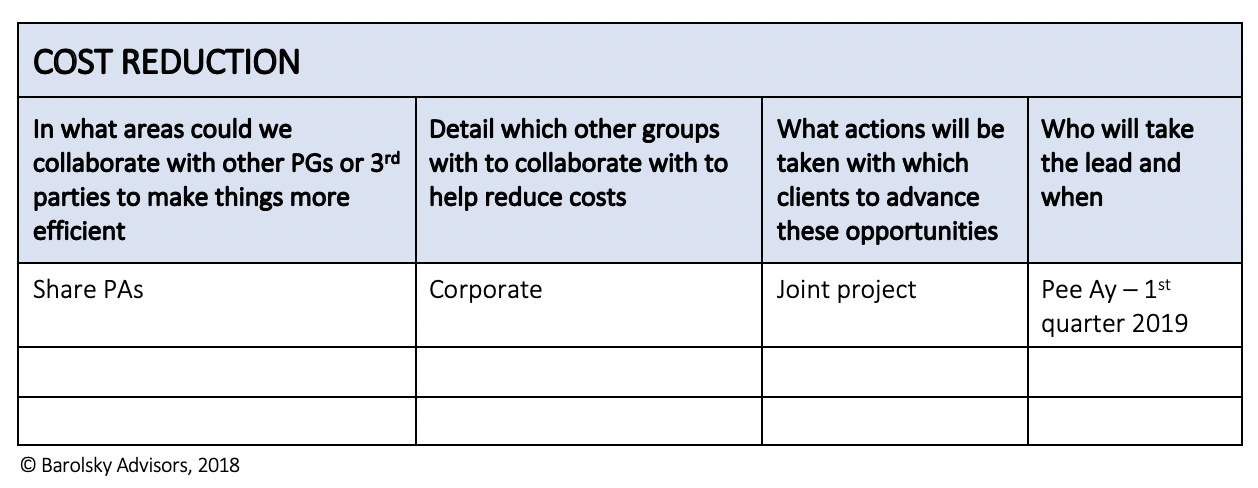

What’s your Collaboration Agenda?

In Articles, Commentary on 19 October 2018 at 9:11 amThe benefits of deeper collaboration within professional service firms are well documented. One practical idea to advance implementation is to get each practice group to complete their Collaboration Agenda.

Here’s an Agenda planning template (with a worked example) for you to use and adapt:

‘Top-down’ and ‘Bottom-up’

I observe that collaboration opportunities are identified both the centre and within practice group themselves. As such, it useful for the FIRM’s leaders to have the first attempt at listing collaboration opportunities, and then for PRACTICE GROUP’s to respond by adding to and refining this list.

Source: strikingly.com

Transitioning your low-profit clients, aka saying 4Q to the Q4s

In Articles, Commentary on 11 May 2018 at 1:21 pm“Manage customers for profit, not just sales”, recommended Harvard’s Benson Shapiro in his famous HBR article way back in 1997. Three decades later, many law and accounting firms still haven’t got the message. Yes, revenue growth is really important in firms with high fixed-costs, but paying lip-service to client profitability is a major missed opportunity.

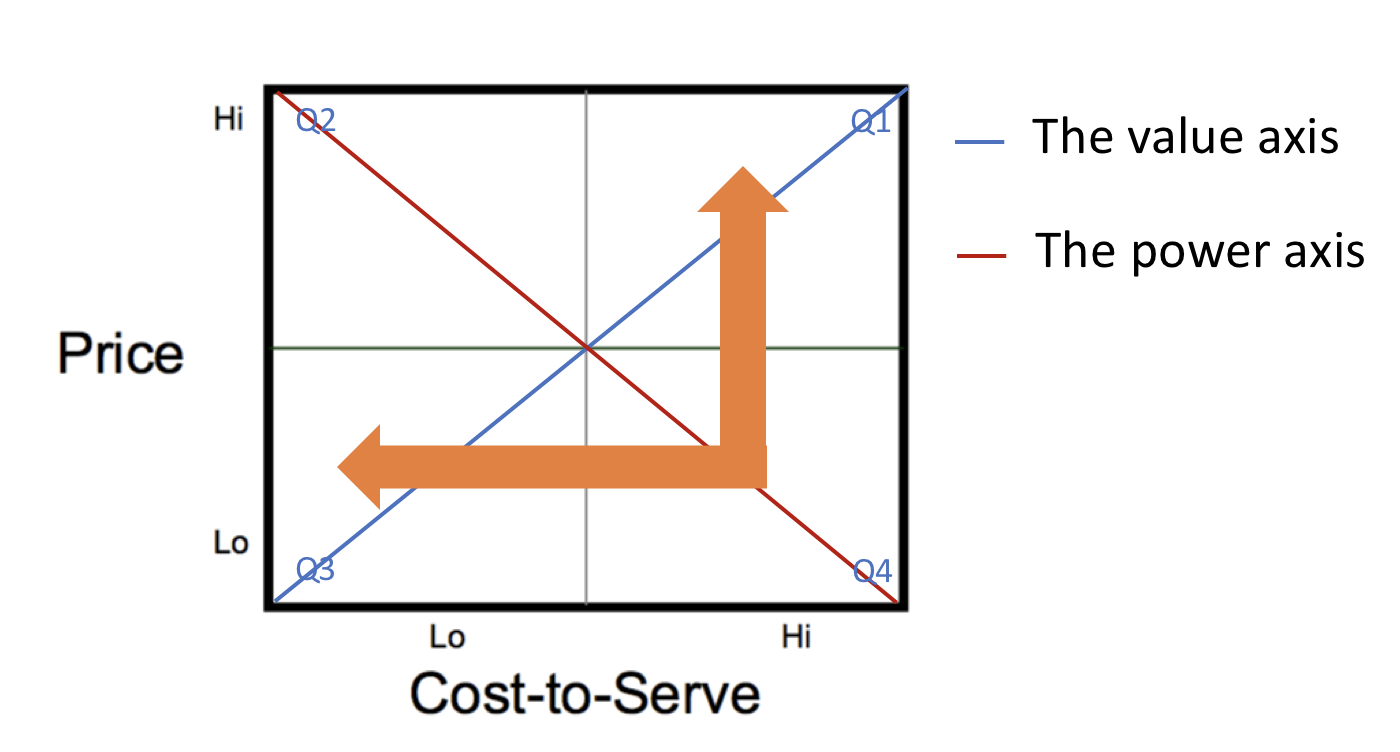

The Client Profit Matrix

Shapiro and his friends offered a useful tool to map your firm’s client portfolio. On the vertical dimension is relative price and on the horizontal is relative cost-to-serve, as illustrated below.

The Q1 Hi Price Hi Cost segment has those clients purchasing new-to-the-world offerings which require senior practitioner input and bespoke processes. It also includes those clients requesting full-service ‘turnkey’ solutions.

The Q2 Hi Price Low Cost segment includes those clients that think the best of you and that really value your services. Q2 also includes uninformed purchasers and unchallenging price-takers.

The Q3 Low Price and Low Cost segment are the bargain-hunters, no-frills and commodity buyers.

Q4 Low Price High Cost include those high-revenue (often labelled “strategic”) clients who leverage their bargaining power and demand value-adds, special services and reporting. It also includes the soul-destroying clients that require an inordinate amount of handholding. The third group, the ‘tail’, are very small clients that barely cover the costs of account establishment and maintenance.

The Power Axis and the Value Axis

Over time, Q4 clients are not sustainable. A special effort needs to made to move these clients closer to the value axis, the blue line in the chart where value is shared roughly equally in the exchange between the firm and the client.

The red line in the matrix is called the power axis. The part of the line in Q2 is where the firm has relative power over its client and bottom right Q4 where the client has more power than the firm.

Transitioning Q4 Clients

There are five broad strategies dealing with Q4 clients:

1. Reduce cost-to-serve – offer similar client benefits but deliver them at a much lower cost. This approach might include a combination of redesigning delivery processes, switching to lower cost resources, automation and cost-transfer i.e. get the client to do more. The banks’ strategy of shifting basic transactional banking services from retail branches to the web and smartphones is a brilliant example of this.

2. Service augmentation – create new higher value products and services and charge more for them. Part of this approach is to develop a deep understanding of which specific elements of value are important and tailor the offer accordingly (see this post for more). Branded technology companies are particularly adept at charging their customers premium prices for new models and inventions.

3. Unbundling – demarcating different product-markets along the value axis and negotiating different prices for each. The Big 4 accounting and consulting firms are quite adept at charging eye-watering hourly rates for their top corporate tax advisors while charging the same clients low fixed fees for commoditised compliance services.

4. Renegotiating – approaching the client with an open-book and requesting the relationship to be reset with a pricing and cost structure that’s fairer and more sustainable. There are many examples where new ‘co-created’ solutions yield better outcomes for both client and firm, but also strong incentives for long-term efficiency gains and innovation. The Perkins Cole-Adobe model is one recent example of this.

5. Say goodbye – if all else fails saying, “4Q” to Q4 clients is the best option. Retaining a value-destroying client over time is clearly not in the firm’s interest and walking away is the bravest and smartest thing to do. Gifting soul-destroying clients to your competitors can make you stronger and them weaker. There may be opportunities to transfer Tail clients to other providers better suited to meet their needs, in return for ‘right’ client referrals.

Client life cycles and migration paths

The Client Profit Matrix can also be a useful analytical tool to track client migration paths over time. One theory is that a typical client relationship will go from Q1 ==> Q2 ==> Q3 ==> Q4. At the early stages of a relationship, costs and price are higher as the parties get to know each other. As the relationship matures and other firms start to contest the client’s spend, prices start to drop. Over time, cost-to-serve rises as more bells and whistles are added.

Clearly, service innovation and better value communication are essential in slowing down this maturation cycle and keeping clients in the top-left of the matrix for longer.

The underlying intent of a ‘loss-leader’ strategy is to go quickly from Q3 ==> Q2 or Q1. It is interesting to track how many of the clients, in fact, make that move and what facilitates this migration. One recent example of this comes from Allens-Linklaters who acquired Canva via its low-cost, low-price online Accelerate platform. They recently reported helping Canva to grow to a $1 Billion market valuation.

Doing a longitudinal heat map of the Client Profit Matrix can be a very useful tool to track your firm’s overall strategic health. In the graphic below, one can clearly see the firm is losing ground and becoming weaker over time.

Call to action

Have a go at mapping your firm’s client portfolio. It will reveal your entrenched Q4s and force an honest strategic discussion as to which of the five transitioning strategies to pursue.

What law and accounting firm clients really care about

In Articles, Commentary on 28 February 2018 at 8:19 amLast week, Bain published a simply brilliant article in the Harvard Business Review exploring what B2B clients really care about. There are so many rich insights and applications for law and accounting firms, including five practical ideas described in this post.

40 Value Drivers

The Bain framework presents 40 ways in which your firm can create value for its clients, categorised into five areas: Table Stakes; Functional Value; Ease of Doing Business Value; Individual Value and Inspirational Value.

Five practical ideas to use in your firm

Idea #1: Have value conversations

Sit down with your client, take out the 40 Value Drivers diagram and ask them to identify the most important value drivers for them personally, their team, their procurement department and their organisation more broadly, and why?

During the conversation explore which value drivers are likely to be more important in two years time.

Get your client to evaluate your firm’s current service offering and relationship and how it compares with key competitors. Use it to explore opportunities to create more value and to test ideas for new offerings. Ask what they’d be prepared to pay more for? Ask what they’d prefer not to have if it meant a lower overall cost?

Idea #2: Re-clarify your value proposition

Your value proposition (VP) is your promise of value to clients. Your VP should be perceived to be superior to clients’ other choices and deliver a sustainable return.

At a firm level, you may wish to explore which of the 40 drivers are core to your firm’s VP or brand promise. Do you go wide and promise lots of things, or go deep and promise one or two things better than anyone else?

Next time you’re pitching for work or writing a tender document, use the framework to get real clarity of your unique selling proposition or USP.

Idea #3: Reassess your firm’s purpose

How does your firm’s current purpose statement measure up in the Inspirational Value category? Does it inspire and truly resonate with stakeholders?

Your firm is a combination of a private enterprise delivering profits to its owners and a social enterprise delivering a broader community benefit. There is an emerging generation of clients and staff that connect much more deeply with a firm purpose that reflects both social and financial outcomes.

In an era where true differentiation based on service and quality is almost impossible, there’s a good chance Inspirational Value will become the battleground of the future.

Idea #4: Foster creative thinking

Running a hackathon, design thinking or ideation workshop? Go through each of the 40 value drivers and explore three or four fresh ideas in each. Deep diving around the client and their needs is always a great place to start.

Idea #5: Update your CRM

Tweak your CRM to make sure you capture insights around what your clients really care about and what drives value for them. Add five new fields to your CRM around the five categories of value creation with drop-down menus of each element and comments.

Your ideas

I’d love to hear your ideas on how to use this brilliant new model.

Source: strikingly.com

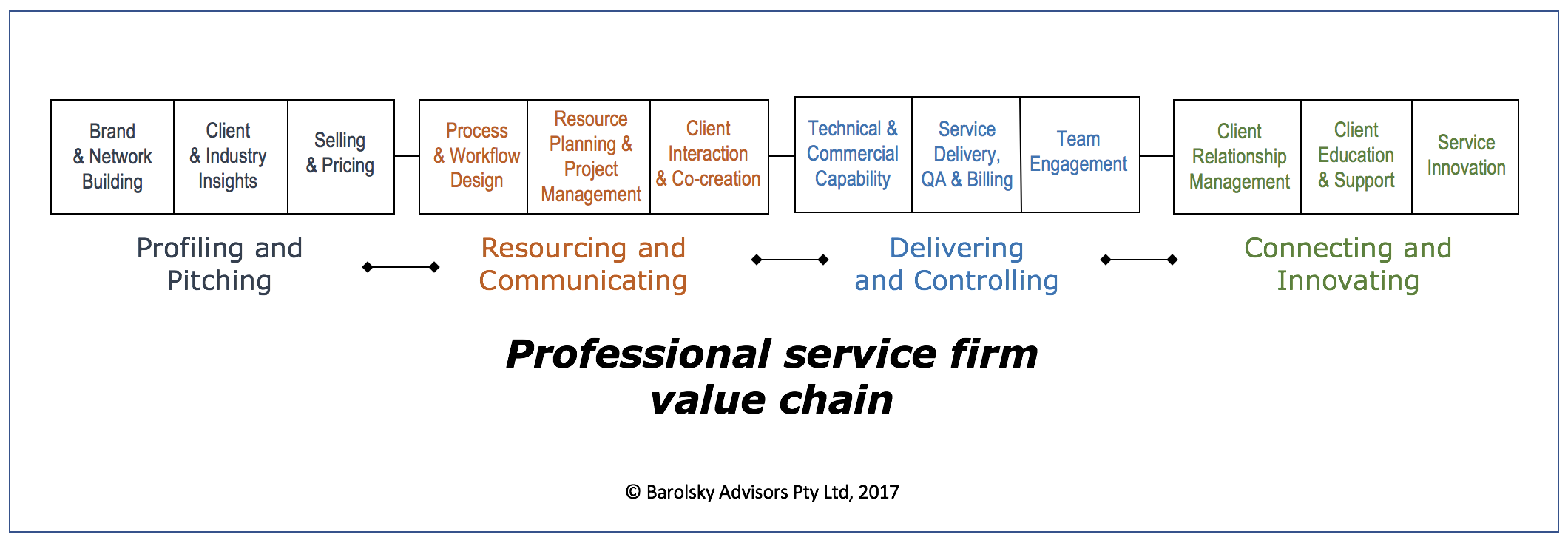

A professional services value chain

In Articles, Commentary on 31 August 2017 at 2:00 pmMichael Porter’s famous value chain did NOT have me at hello. I’ve never found it a particularly valuable tool in crafting professional service firm strategy. Most firms don’t talk about “Inbound and Outbound Logistics” or have “Procurement” as a major support function. Distinguishing between “Operations” and “Service” in a service business is just plain confusing.

In the spirit of further developing the theory of the professional service firm, here’s my go at a professional services value chain…

WAYS TO ADD VALUE

Firms can add to their profitability and competitiveness (my definition of adding value) in the following ways:

#1 Profiling and Pitching

- Brand and Network Building – branded premium providers command higher prices and attract top talent. Firms with better networks spend less on mass marketing and get more low-cost referrals.

- Client and Industry Insights – firms that really understand their client’s business and industry have better bid-win strike rates and a higher percentage of sole-sourced work.

- Selling and Pricing – firms that are adept at selling and pricing capture more value, discount less and win more.

#2 Resourcing and Communicating

- Process and Workflow Design – firms that have streamlined workflows use fewer resources for the same outputs. They generally have faster and more predictable response times and enjoy lower error rates.

- Resource Planning and Project Management – significantly higher margins can be realised by configuring the right combination of talent, tools and technology for each matter or project. More and more clients are choosing firms based on their ability to plan and project manage their work.

- Client Interaction and Co-creation – better client communication and engagement usually increases the chance of client satisfaction and value perceptions. These, in turn, improve client loyalty, pricing and billing outcomes.

#3 Delivering and Controlling

- Technical and Commercial Capability – firms that are perceived to provide better quality and more commercially relevant advice are usually able to command a price premium.

- Service Delivery, Quality Assurance (QA) and Billing – firms that are able to deliver efficiently, effectively and consistently usually outperform their peers. So too are those that bill and collect fairly and promptly.

- Team Engagement – firms that can motivate and inspire their staff will usually enjoy higher productivity, better quality work and less regrettable turnover.

#4 Connecting and Innovating

- Client Relationship Management – firms that have wider and deeper relationships with their key clients will usually enjoy lower business development cost, higher share-of-wallet and more predictable revenue flow.

- Client Education and Support – firms that support their clients through ongoing education and other activities relevant to their needs will enjoy better client relationships and loyalty. Informed purchasers often brief better, respect their providers and know what they don’t know.

- Service Innovation – firms that continue to evolve their service offering to address new market needs will retain current clients and attract new ones. Innovation that lowers costs will give firms more price-setting discretion.

USING THE MODEL

Where to invest

Source: Dreamstime

The value chain model can be used to assess where resources are currently deployed and where they should be. For example, most law firms put a lot of time and energy into just five areas: Brand and Network Building; Technical and Commercial Capability; Service Delivery, QA and Billing; Team Engagement and Client Relationship Management. This means that seven other value-adding areas are potentially sub-optimised. A more deliberate focus in each of these areas could add up to a significant improvement in profitability and competitiveness.

Where to innovate

Many professional service firms are looking to innovate and “digitise” their business. The model can be used to determine what elements of the value-chain should be the focus of change and investment. For example, rather than spreading themselves too thinly, a firm might want to focus their energy and dollars on getting closer to their key clients and enhancing client connectivity and engagement. This would mean an emphasis on Client Engagement and Co-creation, Client Relationship Management and Client Education and Support.

What should we make, buy or borrow

By analysing its value chain, a firm can decide which elements it should make, which it should buy, and which it should borrow. So, for example, one of my accounting firm clients has engaged a specialist lead generation company to help out with Sales and Pricing. They recognised that prospecting for new clients was a key weakness, and that re-training the firm’s partners would be like flogging a dead horse. They pay the consultancy $500 for each meeting they set up within defined ‘right client’ parameters.

How do we compare

The value chain model can be used for head-to-head competitor analysis. Further insights can be gained by examining each of the 12 areas, assessing where a firm is ahead, where it’s at par, or where it’s behind its key competitors. A firm can then use the model to decide its core strategy, that is, how it’s going to win and what capabilities will be needed for success. For example, if very few direct competitors are focusing on Resource Planning & Project Management, this might be a source of competitive advantage in the period ahead.

How do we organise

The final application area of the value chain model is to ensure there is oversight of each of the value-adding areas or categories. For example, a firm may elect to create a Resourcing and Communicating SWAT team, with a blend of Practice, IT, HR, Finance and BD executives, charged with identifying and making improvements.

TO CONCLUDE

I’ve stuck my neck out and come up with an alternative value chain model. What do you think?

Sorry, Michael. Nothing personal. Just business. Professional service firm business.

7 key enablers of smart collaboration

In Articles, Commentary on 10 March 2017 at 7:27 amIn January 2017, Harvard professor and ex-McKinsey consultant, Heidi Gardner, published Smart Collaboration. The book describes the results of her 10-year study into the benefits of collaboration in professional service firms. Gardner concludes that firms that effectively integrate cross-team solutions to solve clients’ problems will significantly outperform those that just rely on cross-selling solo-specialists:

The book is great in making the case for collaboration, but is a little thin when it comes to the “how to” bit. This post is my take on execution, and describes seven key enablers of smart collaboration…

#1 The right clients

The business case for collaboration is much stronger when your firm is servicing [i] large client organisations, [ii] with complex and diverse needs, and [iii] relatively sophisticated approaches to purchasing professional services. For instance, a small monoline insurer with a cab-rank panel structure would not be a prime prospect.

#2 Capability breadth

Gardner states that the true benefits of smart collaboration come from combining the skills and experience of a range of different practitioners to solve the client’s most pressing problems. This multi-disciplinary approach is hard to copy, is less price sensitive and much more fun to deliver.

It follows, therefore, that firms need to have service depth AND breadth for collaboration to payoff. Larger full-service firms would have relatively more opportunity than others.

#3 A culture of “our” client, not “my”client

In many firms, the prevailing culture is one where client relationships are primarily owned by individual partners, rather than seen as assets of the firm. In these instances, distrust of colleagues to serve “their” clients is more common than not. Trying to facilitate smart collaboration in a deeply individualistic culture is a long and hard road.

Many of the professional service firms I work with think they are collaborative, but in reality they’re collegiate. The latter describes a club of friends happy to socialise together. The former describes a one-firm firm where everyone is hardwired to win and deliver together.

Many of the professional service firms I work with think they are collaborative, but in reality they’re collegiate. The latter describes a club of friends happy to socialise together. The former describes a one-firm firm where everyone is hardwired to win and deliver together.

#4 Great client leaders

Client Relationship Partners work across practice teams to bring the best of the firm to the client, and the whole of the client to the firm. These boundary-spanners are crucial in growing the network of relationships between the firm and the client. Success is more likely if the firm empowers this important leadership role, and invests in developing its client leader talent pool.

#5 Effective client knowledge sharing

Gardner states that a “collaborative technology platform” is essential in connecting partners with the right opportunities, as well as mitigating some of the obstacles to collaboration. While I broadly agree, many firms fail to get a positive return on their CRM investments, not because of technology issues, but because the cultural and strategic settings don’t facilitate communication and knowledge sharing.

Collaboration is enhanced by partners having a good understanding of [i] the firm’s full capability set, [ii] the client’s context and needs, and [iii] the details of the firm-client interaction.

#6 Consistency in energy and standards

The outcomes of a team are significantly enhanced when all team members have similar service standards. Problems arise if one team member thinks a “responsive” email reply is 24 hours, while another thinks its 24 minutes. It also helps if all team members have a similar drive to succeed and share common values around client focus.

There are two schools of thought around consistency of service style. Those who argue for a house-style cite benefits of a seamless client experience, resource fungibility and delivery efficiencies. The contrary view is that differences in style facilitate diversity and creativity. I’m more in the latter camp.

#7 The right measures and rewards

In the words of Peter Drucker, “what gets measured gets managed”. In the words of James Goldsmith, “if you pay peanuts, you get monkeys”. If the firm incentivises solo-specialist behaviours and outcomes, the chances of meaningful collaboration are exceedingly low.

Call to action

Gardner’s research clearly illustrates the benefits of smart collaboration over cross-selling. If you sense the potential in your firm: [i] write down each of these seven enablers; [ii] give your firm a score out of 10 on each, and [iii] identify the key actions to shift the dial in the next six months, and closer to a 10 over the next 36 months.

There are two words in “strategic plan”

In Articles, Commentary on 3 February 2017 at 6:53 amSome strategic plans are heavy on plans, but light on strategy. Some have beautiful strategy descriptions and diagrams, but no roadmap for execution. There are two words in “strategic plan”, and you need both of them.

The strategy bit

The strategy bit

Lafley and Martin (Playing to Win, Harvard Business School Press, 2014) suggest strategy is about describing an integrated and coherent response to five key questions:

- What are our winning aspirations?

- Where will we play?

- How will we win?

- What capabilities are critical to our success?

- What systems and enablers are required?

From my experience, this model works extremely well in professional services. It’s simple, practical and not overly jagonised. It can be used at multiple levels – the firm overall, for practice groups and individual practitioners. When challenged by a sceptic there’s a strong body of research evidence to support it.

The plan bit

The plan element describes your strategic priorities, where you will (and won’t) be investing, what key initiatives will be actioned, who, when and how things will be done. There are five frameworks that you might find helpful to organise and present your thinking:

#1 McKinsey Three Horizon Growth Model – listing key strategic initiatives around the expected timing and certainty of benefit. H1 is around defending and extending core business; H2 building the momentum of emerging new business; and H3 creating options for future business. The graphic below illustrates the use of the Three Horizon model in a strategic plan for a key client.

#2 Kanban Boards – a visualisation tool that enables you to categorise and optimise the flow of work, be it a specific project, a program of work or a major strategic initiative. This agile-friendly tool is brilliant for cross-firm collaboration, accountability and transparency. The graphic below shows a Kanban Board, using Trello software, for a specific strategy project.

#3 Strategy Roadmaps or Infographics – expressing the strategy in the form of a journey, noting key events and milestones on the way. When the strategy is expressed as a narrative, one often finds there’s much greater understanding and buy-in. The graphic below shows a roadmap for an innovation strategy.

#4 Past Present Future – detailing the specific things that will be changed and those things that will be preserved. This is a simple device to explain the implications of a particular strategic direction. The graphic below shows the changes an engineering firm is seeking in adopting a client-centric strategy and culture.

#5 Strategic Pillars – a graphic device summarising the key areas that will be focused on in strategy execution. The symbolism of the pillar model is that each component is necessary for success – missing one pillar compromises the integrity of the whole. The graphic below shows a pillar model for a strategic account management program.

Call to action

Take a quick look at your current strategic plan and ask yourself these three questions:

- In light of market, client and competitor trends over the next few years, have we put enough thought into where will play and how we will win?

- Are we crystal clear on our major priorities, investments and actions?

- Have we presented our strategic thinking in a coherent and compelling way?

If the answer is ‘not really’ to any or all of the questions, then it’s appropriate to invoke another famous two-word phrase: IT’S TIME.

The Taxi Taxonomy – four things to learn if you’ve only got a taxi ride to prepare

In Articles, Commentary on 14 June 2016 at 12:06 amYou’ve got a meeting with a prospective client and you’ve left your preparation to the last minute. What are the ESSENTIAL things to learn during your taxi ride on the way to the meeting?

The Taxi Taxonomy, presented in the two-by-two below, is a client analysis cheat sheet. It is no substitute for more in-depth preparation, but provides a useful start to the intelligence gathering process. The Taxonomy suggests classifying your analysis into four Ps (to make it easier to remember):

- Profit drivers* – the revenue, cost and other strategic priorities of the organisation;

- Political drivers – the cultural and political state of the organisation;

- Position drivers – the role and requirements of the person you’re about to meet; and

- Personal drivers – their key personality attributes and preferences.

There is a continuum of data ranging from the overt to the obscure. The overt can usually be ascertained from web and social media searching. Obscure data most often comes from speaking with those with direct first-hand experience, including employees, clients, suppliers or business partners.

The Taxonomy in Practice

A client of mine gets her business analyst to prepare a one-page Google Doc summary based on the four quadrants in the Taxonomy before every client meeting. With repeat clients much of the data is the same but any new items or changes are highlighted. She then updates the Google Doc with new or fresh insights after each visit. Ironically this is usually done on her smartphone during the taxi trip back from the client.

MBA IN A DAY

For those interested, I will be expanding on this framework and presenting many others at a forthcoming public seminar called MBA IN A DAY. The seminar is targeted at mid-career lawyers looking to enhance their knowledge of business and develop a deeper understanding of their clients and prospects. Many lawyers are experts in the law but have received very little training in business. Click here to read more: http://mbainaday.strikingly.com/

Source: Fotolia

* For non-profit organisations and government agencies, this quadrant might be reframed as Purpose drivers, and include things like social charter, development strategy, cost and operational priorities and H2 and H3 opportunities.

culture, key account management, Leadership capacity, professional service firms, Sales management, strategy management

Why Harvard is wrong on law firm management

In Articles, Commentary on 11 November 2020 at 10:17 amFull text of my opinion piece first published in the Australian Financial Review on 5 November 2020

Bob Andersen is a hands-on, high-billing, star partner at the Cambridge Consulting Group. He also has deteriorating relationships with his fellow partners, his team members and his family.

Anyone who has been through Harvard Business School’s Professional Services Leadership program knows Bob well. The Cambridge case study is used to illustrate the tensions in the role of partner in being both a successful ‘producer’ and busy ‘manager’. The producer builds relationships, wins new business and services clients and the manager internally oversees operations.

The Harvard faculty make much of the producer-manager concept in distinguishing professional services from other types of organisations.

But it’s time for Harvard to update their thinking and refine their language – the role of partner in the modern law firm is much more an adviser–owner–leader.

Business owners

The Harvard model is silent on ownership – a core tenet of the law firm partnership model – yet from day one, most new partners are told they need to think and act as proprietors.

This aspect of the role typically includes taking stewardship of the firm’s assets (including its IP), role modelling its values and brand, building its relationship capital by sharing clients and connections, helping set the overall firm direction and risk profile, and showing public support for agreed firm investments and initiatives.

Adoption of a business owner mindset applies to all partners regardless of financial stake. Both equity and non-equity partners have ‘partner’ on their business card and that means the same thing to all stakeholders outside of the partner group.

More leaders than managers

The Harvard model also seems to emphasise management over leadership.

Leadership is about setting directing, inspiring action and facilitating change. Management focuses on creating order and efficiency. Both are needed, but effective leadership is very often the critical difference in a legal practice going from good to great.

Law firm partners take on roles that include a mix of team, sales, thought, project and client account leader.

Good team leaders facilitate a process of crafting strategy which describes the team’s purpose, objectives, operating standards and where and how the team will compete. Strategy implementation is enabled by the communicating clear expectations, providing support, holding people to account, giving and receiving ongoing honest feedback and removing roadblocks.

As sales leaders, partners must ensure there’s enough revenue coming in the door to cover costs and meet or exceed targets. This means active ongoing prospecting for new work opportunities and converting a healthy share of client proposals into paid work.

A common approach to sustainable revenue generation is for partners to become well-known as an expert or thought leader in a specific area of law and/or client sector. In this role, thought leaders generate valuable content that can be used in marketing communications, events and client pursuits.

Most partners will also have a responsibility to protect and grow key client relationships. For large, multi-practice clients, the job goes beyond good client service. They must act as client account leaders to drive value creation across the board for both the client and the firm.

The adviser-owner-leader construct provides a more comprehensive and accurate description of the modern partner role. Doing it all and doing it all well is probably a stretch for most partners in your firm, but stretch is better than stagnation.

It takes a bit of chutzpah to claim Harvard is out of date. But in this instance, I think I’m right.

Share this: